Gold and gold stocks bull analogs

Gold and gold stocks bull analogs

Jordan Roy-Byrne – mining.com

http://www.mining.com/web/gold-and-gold-stocks-bull-analogs/

Over the past two weeks the precious metals complex has retested its Brexit breakout and rebounded back to the July highs. Today’s jobs report has pushed the complex lower but has delivered an opportunity to cash heavy portfolios which have missed the bulk of the move. With that said, we wanted to share our current analog charts for Gold, gold stocks and junior gold stocks which suggest continued upside potential in the sector.

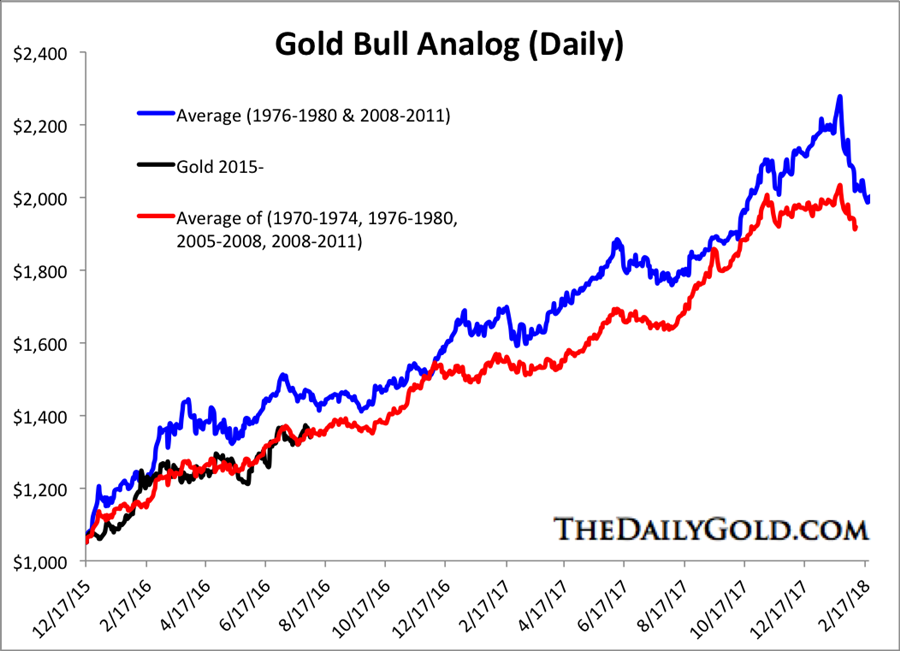

The first chart plots the current rebound in Gold compared to the average of its two strongest cyclical rebounds (1976 and 2008) and the average of four rebounds (including 1976 and 2008) within its secular bull markets. As we can see, the current rebound is closely following the average of the four rebounds. If Gold continues to follow that path then it could reach $1500/oz before the end of the year and retest its all time high of $1900/oz by the end of next year.

Turning to the stocks we find that the large miners are fairly extended at present. The HUI is currently above the other two rebounds. If the HUI continues to follow the path of the last cyclical bull market (2008-2011) then it has somewhat limited upside. However, considering my research and analysis, the recent low in gold stocks figures to be quite a bit more like the 2000 low. By following that path the miners could triple over the next two and a half years.

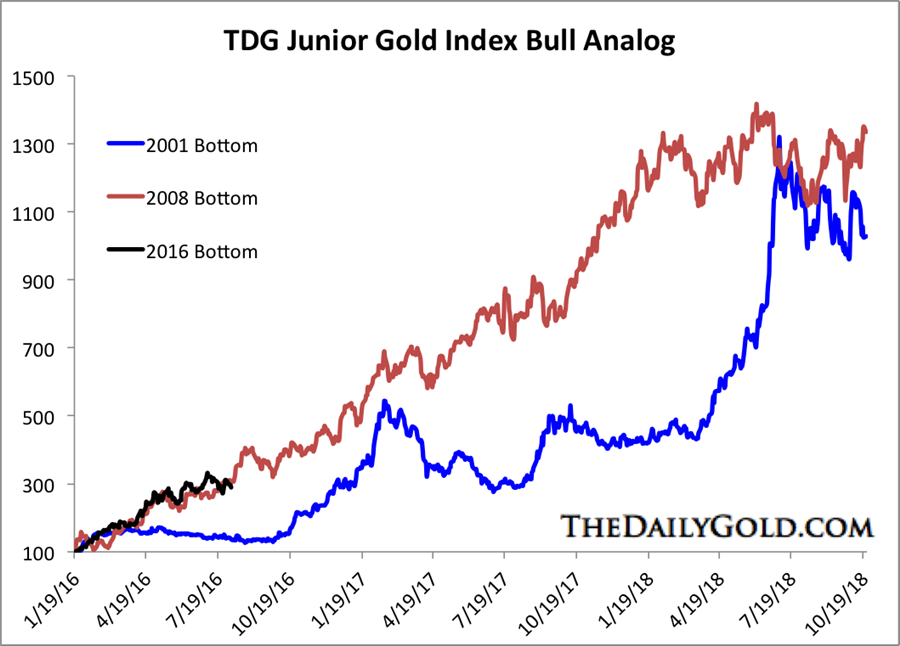

My own research and discussions with industry sources (folks with more experience and knowledge than me) leads me to believe the best value is currently in the juniors and the smallest juniors. My junior index bull analog chart shown below confirms that view. My index has already tripled but has plenty of upside potential over the next six months and two years.

Thus far Gold and gold stocks appear to be tracking history quite well. If the bull market continues then these charts should continue to provide some context as to where things could go. History is a very good guide but it is not perfect. No indicator by itself is infallible. In addition to historical analogs we also employ technical analysis, intermarket analysis and various sentiment indicators. We reiterate our view that precious metals are in the early stages of a cyclical bull market that has a chance to turn into a full blown mania. Our views are always subject to change but we remain bullish over the near term.

View Original: http://www.mining.com/web/gold-and-gold-stocks-bull-analogs/

Is it Time to Buy Junior Gold?

Higher Gold Prices = Big Potential in Junior Gold Stocks

-Momentum Public Relations-

The recent surge in gold prices is being noticed by investors. So far this year, gold pricing has moved upwards by approximately 20 percent. This surge has resulted in a buying spree of gold exchange-traded-funds (ETF) and some upward movement in share prices for a variety of gold mining concerns.

BNN – Gold No Longer the Skunk at the Picnic Says Industry Veteran

The big question is; how will the recent surge in prices impact the prospects of junior gold mining companies?

MARKET CONDITIONS:

Current market realities are providing favorable conditions for gold prices to advance further. The external conditions are certainly favorable given many relatively weak major currencies, low oil prices, low returns on mainstream investments, and general sluggishness of the global economy. Historically, gold prices rise when currency falls and vice-versa. The balancing variable lies with prevailing interest rates. When interest rates rise investors are attracted to the yield and hesitate to hold, store and insure a commodity like gold.

Major stock indexes worldwide have declined, despite efforts by the various central banks to spur growth through lower interest rates. Back in 2011, stocks looked much more stable and appeared to be in full recovery from the declines of 2008 and 2009. In 2013, the Federal Reserve in the US signaled that the era of low-interest rates was ending, and investors moved away from gold.

GOLD – HISTORICAL PRICES:

Gold has experienced substantial price growth in the past 15 years, even when post-2011 declines are considered (see chart below). A few weeks ago, gold rose above its 200-day moving average of $1,130 per ounce and questions are being raised about the potential for further price growth that could mirror the rally that peaked at over USD$1,900 per ounce in 2011.

http://www.cnbc.com/2016/02/16/gold-snaps-losing-streak-rises-above-1200-as-stocks-steady.html

The fact that prices have moved up by 15 to 20 percent so far this year suggests that a sustainable price level of $1,300 to $1,400 per ounce is realistic within the next 12 months. It is entirely possible that the pace of the increases this year may leave the commodity vulnerable to profit-taking which could moderate overall gains. Most market observers believe that the perception of the safety of gold as an investment has returned and that investors who bought in 2012 or 2013 will stand to profit from the rising price of bullion.

IMPACT ON JUNIOR MINING SECTOR:

The current price of gold may cause some understandable optimism in the junior mining sector. However, it is important to underline that the usual business fundamentals still apply. Wise investors will continue to avoid being caught up in pricing euphoria and look at key metrics to assess the viability of each opportunity.

Mining companies with significant extraction operations will benefit in a big way from lower energy costs. However, energy cost savings is likely a temporary windfall. One important consideration is the fact that, if gold prices rise, or stabilize close to current levels, a mining operation with a fully loaded cost of extraction of USD$1,200 per ounce will become a cash-positive proposition in the short-term.

What factors could guide investors? We suggest consideration of two “rules”.

RULE #1: Assets & Grades

Investors still need to monitor the value of a gold producer’s assets project by project. There is no substitute for due diligence in examining the grade of the ore that is being produced and following company updates. Grades that are sufficiently high and can produce good margins at USD$800 to USD$1,000 pit shell will result in positive cashflows in the present market. By using the very conservative “pit shell method” to calculate returns, the scrutiny is on the mine’s engineering plan and not on statements by promoters.

RULE #2: PCM

The rule of PCM highlights three additional elements to consider when assessing the hundreds of junior gold plays as investment opportunities.. The three elements are people, cash, and margin.

Simply put, this means that there is no substitute for the careful assessment of the people who are involved in the venture and their experience, integrity, and expertise. Also, companies need to have enough available cash to sustain their CapEx in the face of short-term price volatility. If they do not have cash they can be put out of business quickly by a market correction or an unforeseen production challenge. Lastly, junior mining concerns that own some higher margin operations will have greater functional flexibility. When prices rise, higher cost operations can be developed while lower cost mines can provide a source of funds to balance the CapEx requirements for more speculative ventures.

- Published in Blog, Equitas Resources, Mining